Buying your first home is often described as a milestone achievement—a blend of excitement, pride, and long-term security. Yet many first-time buyers focus almost entirely on the down payment and mortgage, overlooking a range of hidden costs that quietly add up. These expenses don’t always appear in listings or loan estimates, but they can significantly affect your finances if you’re unprepared.

Understanding these costs upfront can help you budget realistically, avoid stress, and make smarter decisions as a homeowner.

Upfront Costs Beyond the Down Payment

The down payment may be the most talked-about expense, but it’s far from the only one you’ll face before getting the keys.

Closing Costs

Closing costs typically range from 2% to 5% of the home’s purchase price. They cover administrative, legal, and lender-related fees, such as:

-

Loan origination fees

-

Title insurance

-

Attorney or escrow fees

-

Appraisal and credit report costs

-

Recording and transfer fees

These costs are usually due at closing and are often underestimated by first-time buyers.

Home Inspection and Appraisal Fees

Before finalizing the purchase, most buyers pay for inspections and appraisals out of pocket. While these costs may seem minor individually, together they can be substantial.

-

Home inspection: Identifies structural, electrical, or plumbing issues

-

Specialized inspections: Radon, mold, or pest inspections may be required

-

Appraisal: Confirms the home’s value for the lender

Skipping these steps to save money can lead to far more expensive problems later.

Ongoing Monthly Costs You Might Overlook

Your mortgage payment is only part of the monthly cost of homeownership.

Property Taxes

Property taxes vary by location and can increase over time. They’re often rolled into monthly payments, making them easy to ignore until they rise unexpectedly.

Homeowners Insurance

Lenders require homeowners insurance, but coverage levels differ. Premiums may increase based on:

-

Natural disaster risk

-

Claims history in your area

-

Replacement cost of the home

If your home is in a flood or earthquake zone, additional insurance policies may be required.

Utilities and Services

Larger homes often mean higher monthly bills. Costs can include:

-

Electricity, gas, and water

-

Trash collection and sewer services

-

Internet and security systems

These expenses are easy to underestimate when transitioning from renting.

Maintenance, Repairs, and Surprise Fixes

One of the biggest financial shifts from renting to owning is full responsibility for upkeep.

Routine Maintenance

Experts often recommend budgeting 1%–3% of your home’s value annually for maintenance. This includes:

-

HVAC servicing

-

Gutter cleaning

-

Lawn care and landscaping

-

Minor plumbing or electrical repairs

Major Repairs

Even well-maintained homes can surprise you. Roof replacements, appliance failures, or foundation issues can cost thousands and often arrive without warning.

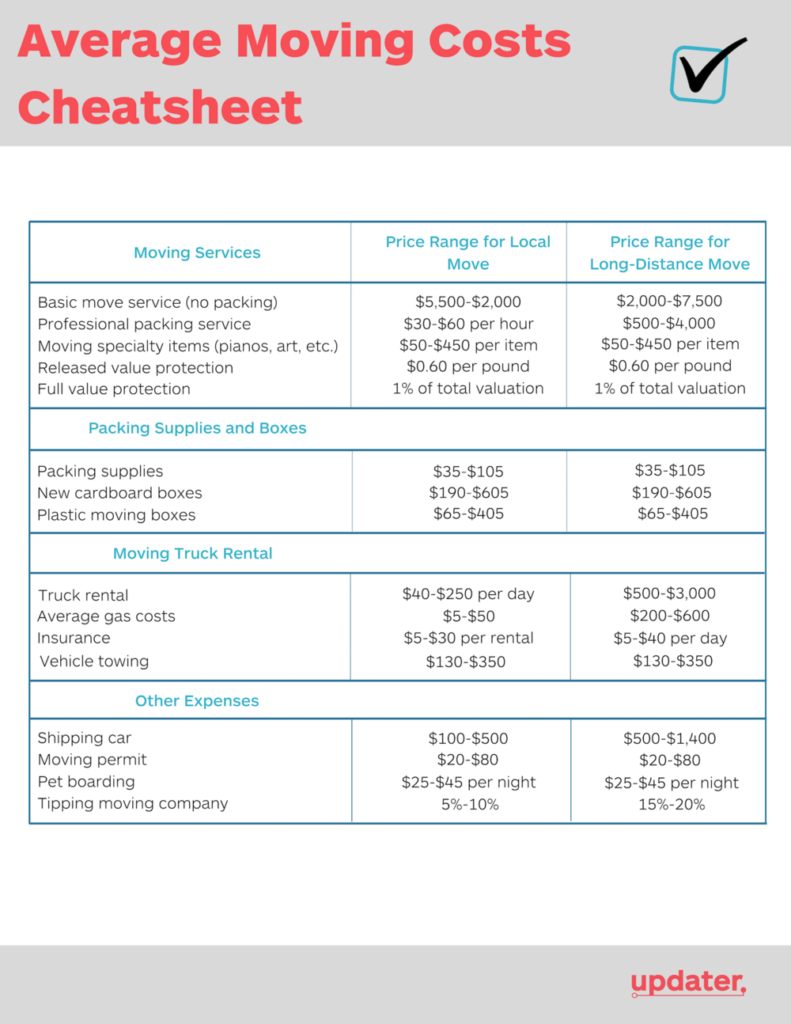

Moving and Setup Expenses

The cost of moving itself is frequently overlooked.

-

Professional movers or truck rentals

-

Temporary storage fees

-

Furniture and appliance purchases

-

Initial repairs or cosmetic updates

These costs tend to cluster within the first few months of ownership, putting pressure on your cash flow.

Lifestyle and Opportunity Costs

Homeownership also comes with less obvious financial trade-offs.

Reduced Flexibility

Selling a home takes time and money. If your job or personal circumstances change, relocating may be more expensive than expected.

Opportunity Cost of Capital

Money tied up in a down payment and home repairs could have been invested elsewhere. While homeownership can build equity, it may limit short-term financial flexibility.

How to Prepare for the Hidden Costs

Planning ahead can turn surprises into manageable expenses.

-

Build an emergency fund specifically for home-related costs

-

Request a detailed loan estimate and review every fee

-

Research average maintenance costs in your area

-

Avoid stretching your budget to the maximum loan amount

Being conservative upfront often leads to greater peace of mind later.

FAQs

1. How much should I budget for hidden home-buying costs?

A good rule of thumb is an additional 5%–10% of the purchase price to cover closing costs, inspections, and early maintenance.

2. Are closing costs negotiable?

Some fees may be negotiable, and sellers sometimes agree to cover part of them, depending on market conditions.

3. Do newer homes have fewer hidden costs?

Newer homes may have lower maintenance initially, but they can still come with higher property taxes, HOA fees, or builder-related expenses.

4. Should I skip a home inspection to save money?

Skipping an inspection can expose you to costly repairs later. It’s usually a short-term saving with long-term risk.

5. How soon do major repair costs usually appear?

Some issues arise within the first year, especially if the home wasn’t well maintained or inspections missed key problems.

6. Is renting sometimes cheaper than buying?

In the short term, renting can be cheaper due to fewer upfront and maintenance costs, depending on the market and personal circumstances.

7. How can first-time buyers reduce financial stress after buying?

Maintaining a cash reserve, avoiding unnecessary renovations early, and tracking monthly expenses closely can help stabilize finances.